Being self-employed

Getting a motorbike is an exciting time, but if you’re self-employed it might be more difficult to get approved. See how we could help today.

Bad credit motorbike finance

No matter what your circumstances are, we believe that just because a person has bad credit, it doesn’t mean they should be denied access to a loan.

Our application process

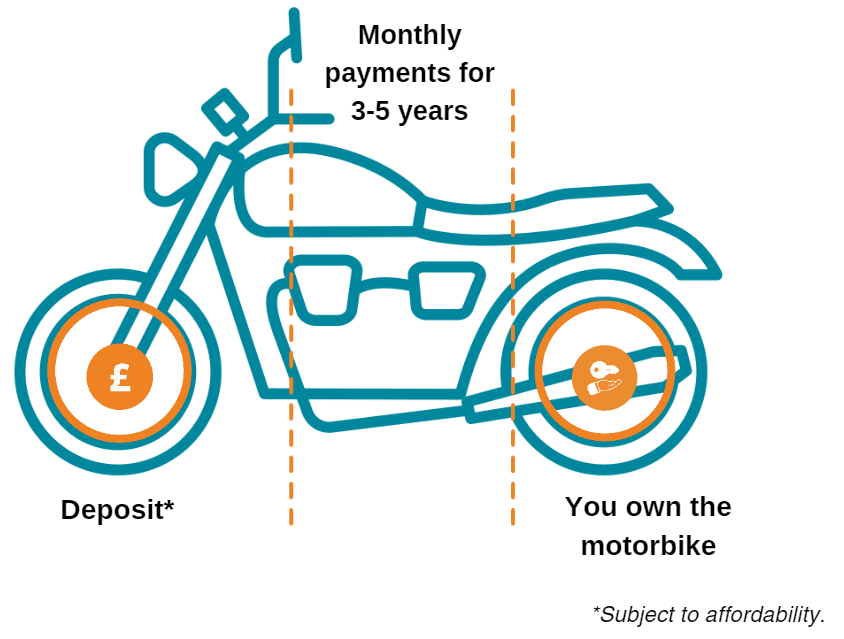

It is important to completely understand the motorbike finance agreement that you may be entering – find out more about how our application process works.