Electric car finance

Looking to buy an electric car? We can help! Find out more about financing an electric car and how it works.

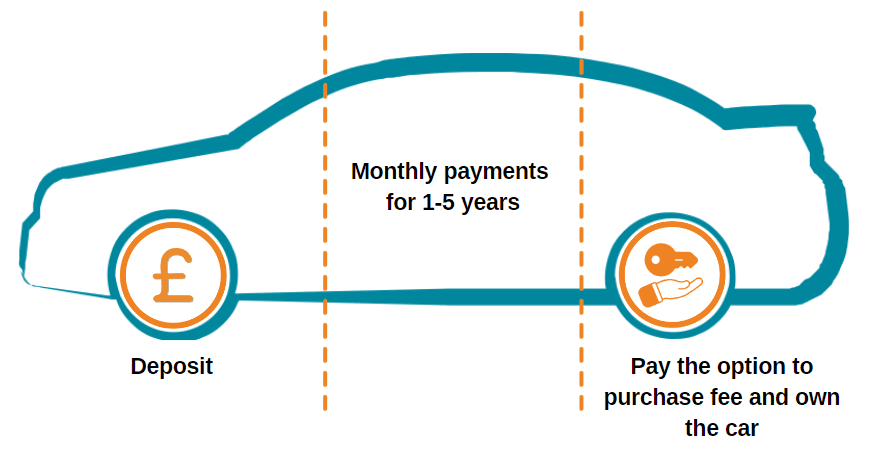

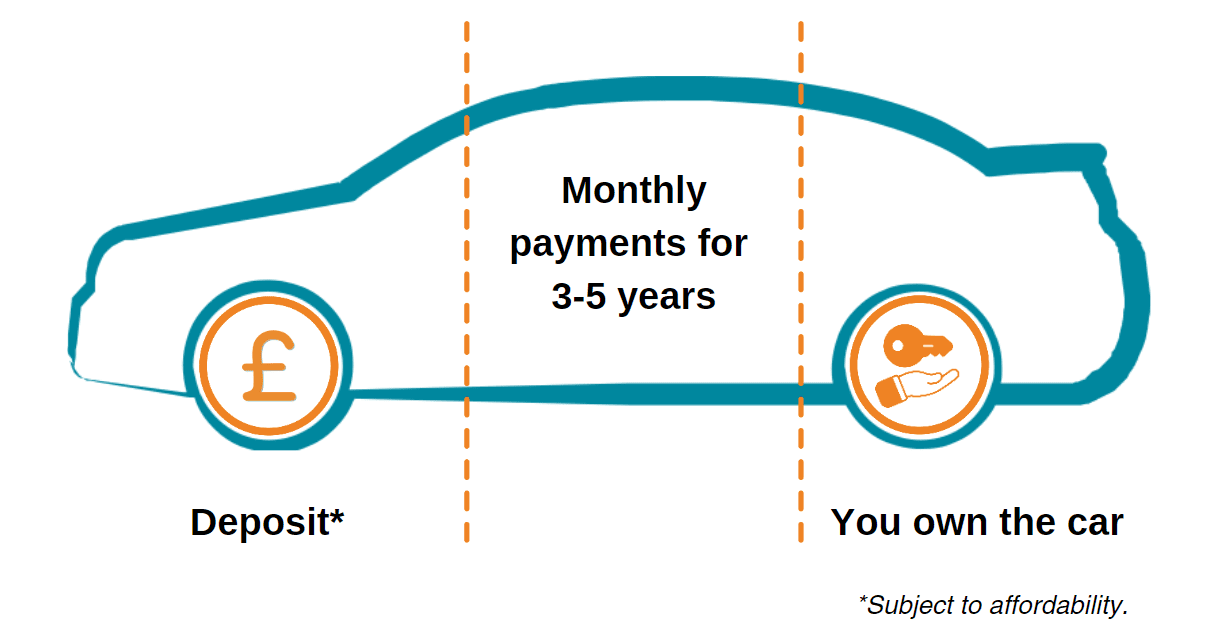

Types of car finance

Understand all the different types of car finance that could be available to you. From Hire Purchase to Leasing.

Our application process

Our friendly experts will help you find the right car from our list of approved dealerships. Find out more about our process.