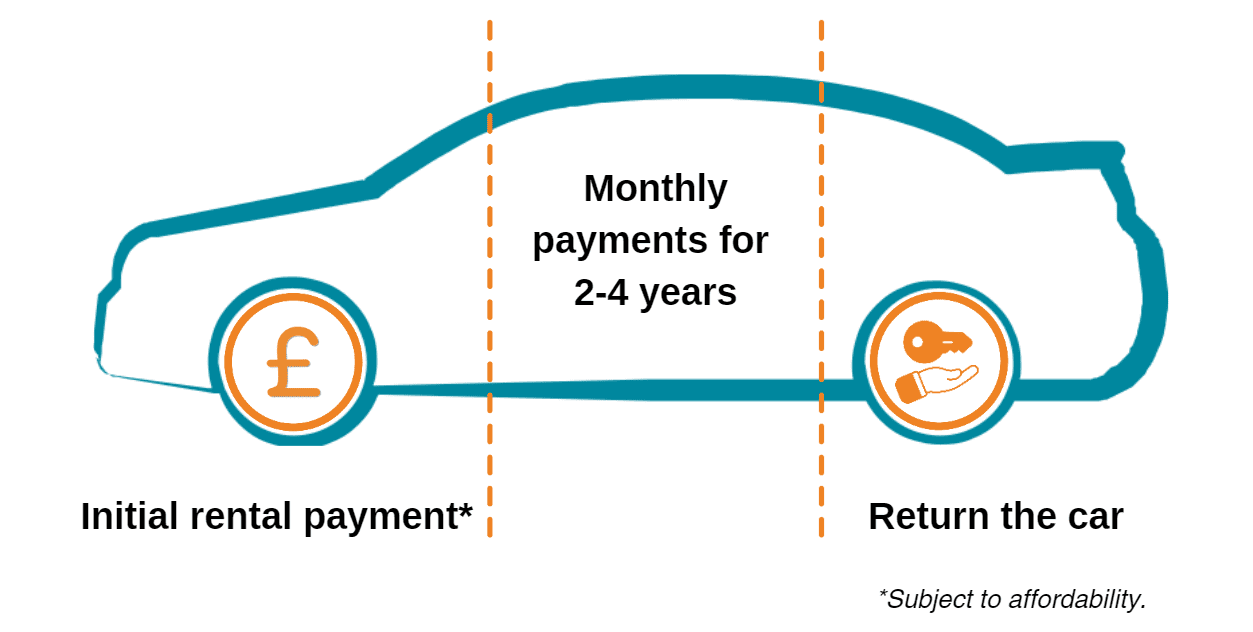

Should you lease or buy?

Leasing is quite different from financing a car. We’ve written a guide that breaks down the differences in more detail, so you can understand what’s best for you.

What do you need to apply?

We don’t offer leasing, we offer Conditional Sale finance. You might be wondering what you need to apply for vehicle finance. Click the button below to find out more.