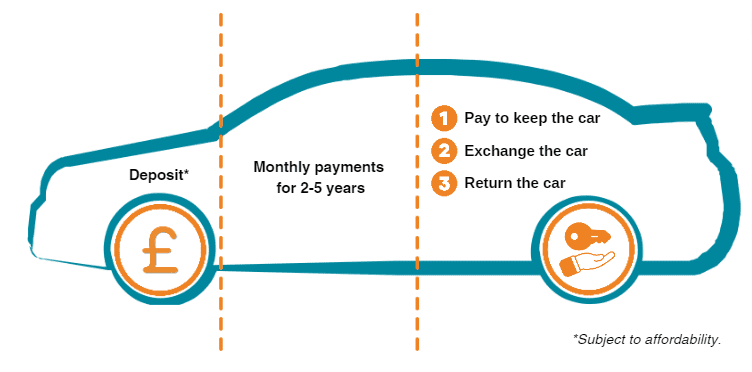

What is CS finance?

Conditional Sale is the type of car finance that we offer at Moneybarn, and it doesn’t always require a deposit.

Types of car finance

Understand all the different types of car finance that could be available to you. From Hire Purchase to Leasing.

Car finance calculator

Try our car finance calculator to see what a CS finance agreement with Moneybarn could look like for you.